A Transfer Pricing report is required to justify that the conditions of the loans between companies of the same group abide by the arm’s length principle (ALP) i.e. are similar to those applied between independent parties.

In practice, the Luxembourgish tax administration may request a Transfer Pricing report in the following main simplified situations:

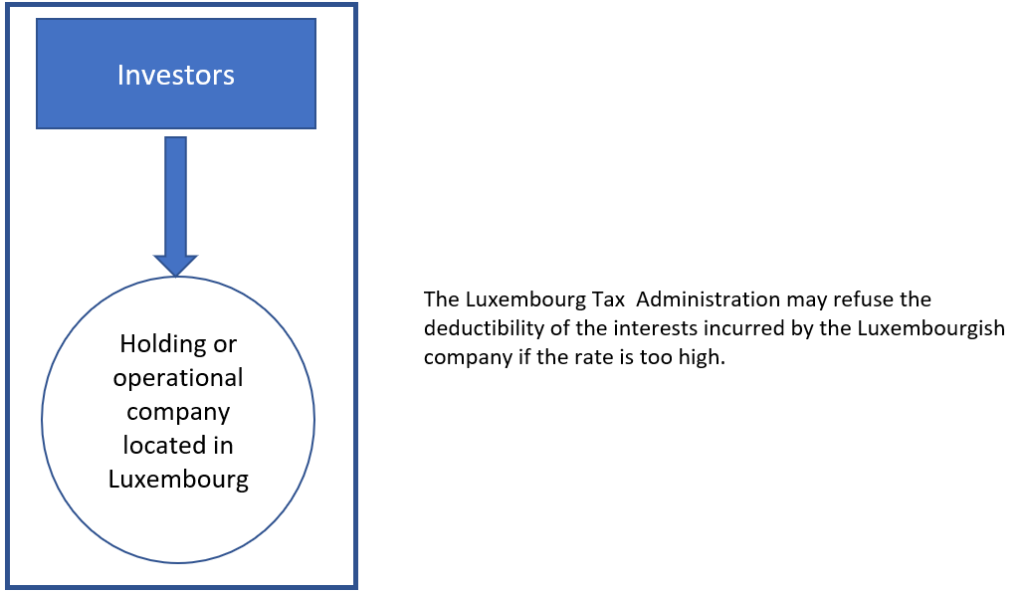

- The Luxembourgish company borrows funds from its shareholder.

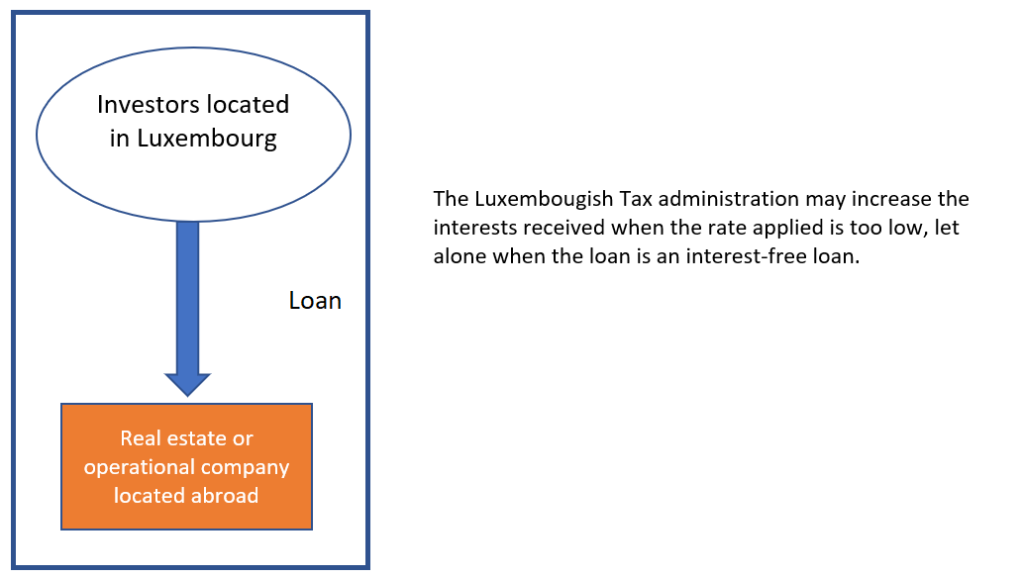

- The Luxembourgish company grants funds to one of its subsidiaries.

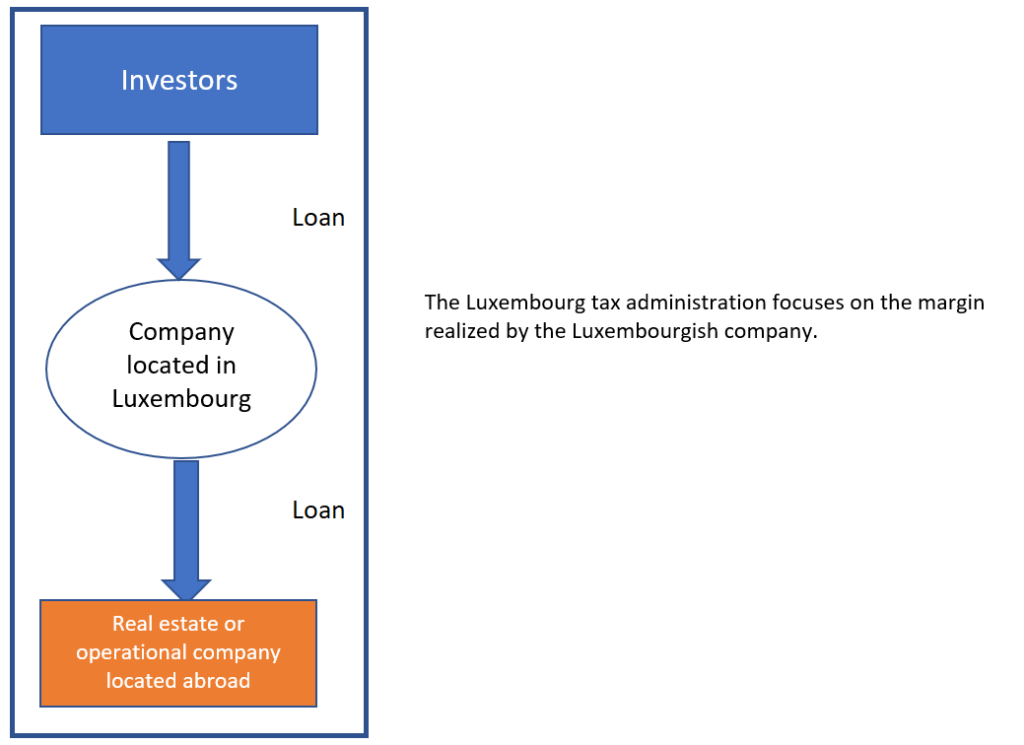

- The Luxembourgish company both borrows funds from its shareholder and grants a loan to one of its subsidiaries.

However, the cost of a Transfer pricing report is usually significant due to the use of databases to justify that the conditions applied are the same as in other contracts concluded by independent companies.

Then, it is quite common that companies raise many questions such as the following ones to avoid such a cost:

Can we reapply the same interest rate as for another “similar” transaction?

Can we apply the same interest rate between the different entities of the same group?

To which extent the rate of an external loan can be used to determine the rate of an intra-group loan?

The answers of these usual questions are not straightforward and request, in most cases, a pre-analysis to delineate in detail your transaction, to appraise your risk and, if need be, to rationalize your financing structure.

This could avoid incurring the expenses of a Transfer Pricing report in some cases by addressing the following questions as well:

Is it financially better to run the risk of a tax audit or to order a TP report?

Can we mitigate the risks by changing the current structure?

Should we care about the effective role of the Directors of the Luxembourgish company?

To which extent are the Transfer Pricing rules applicable if the other companies are resident in Luxembourg?

Whatsoever, you will have in hands the pros and the cons to decide if the cost of a transfer pricing report is reasonable or not!

Please don’t hesitate to contact us if you have any questions or any remarks on this subject – or +352 621 81 73 35.